Distributed energy resources, including rooftop solar, battery storage and electric vehicles, are experiencing significant growth in the U.S. as the power sector evolves to a cleaner, less centralized future.

The U.S. power sector is also seeing rising interest in virtual power plants, which tie multiple distributed energy resources together into one coordinated system.

But what’s propelling the rise of distributed resources, and what are the obstacles to more growth?

This trendline examines the experiences of various utilities, vendors, states and grid operators to provide a comprehensive picture of a burgeoning field at the heart of the energy transition.

New York PSC approves retail and residential storage plan as 6-GW 2030 target in question

New York plans to hold the first of three bulk energy storage procurements later this year as an Aurora Energy Research report forecasts 30 GW of in-state storage capacity by 2050.

By: Brian Martucci• Published Feb. 25, 2025

The New York State Public Service Commission has approved the state’s retail and residential energy storage implementation plan, a significant step in its effort to reach 6 GW of energy storage by 2030.

The Feb. 13 order approved a framework to reach the state’s retail storage deployment goal of 1,500 MW and its residential storage deployment goal of 200 MW. It also includes incentives for resources participating in the New York Independent System Operator’s distributed energy resources program to also be eligible for the retail storage incentive, the PSC said.

Theplan was approved as a new forecast by Aurora Energy Research shows New York falling “marginally short” of its 2030 energy storage target despite an expected deployment surge in the late 2020s, but reaching 30 GW of deployed storage capacity by 2050.

New York’s 6-GW 2030 goal will “support a buildout of storage deployments estimated to reduce projected future statewide electric system costs by nearly $2 billion, in addition to further benefits in the form of improved public health because of reduced exposure to harmful fossil fuel pollutants,” the PSC said in announcing the order.

The 6-GW goal represents a doubling of the previous 2030 goal of 3 GW. It envisions 1.7 GW of new retail and residential storage plus 3 GW of new bulk storage added to about 1.3 GW of existing storage assets being procured by or under contract with the stateas of April 1, 2024, the PSC said on Feb. 13.

Following the adoption this month of its retail and residential implementation plan, the New York State Energy Research and Development Authority expects to make the first of three annual bulk storage solicitations by the end of June for deployment in 2027 and 2028. It plans subsequent storage solicitations in 2026 and 2027 for deployment in 2028 through 2030.

New York has 430 MW of operational battery energy storage capacity as of January, most of it in the central and downstate regions, according to the Aurora report.

Though the average project is 2.5 hours, durations range from 15 minutes to 8 hours, indicating “the state is still trying to figure out the role batteries are going to play,” said Julia Hoos, Aurora’s head of USA East. Shorter-duration batteries generally perform ancillary grid services, while longer-duration installations fill capacity and reliability needs, she said.

Following NYISO’s implementation of Federal Energy Regulatory Commission Order 2023, batteries make up nearly half of the 60 GW of projects in its cluster study process, which evaluates projects in groups rather than individually. Batteries also account for 2.5 GW of capacity remaining in the main interconnection queue, according to the Aurora report. Fifty-five percent of main-queue capacity is expected to come online in 2027 and 2028, and 70% is slated for the congested New York City and Long Island grids, Aurora said.

While the main NYISO interconnection queue is proportionally smaller than the nationwide queue, where capacity awaiting interconnection exceeds total installed capacity, New York’s queued storage projects are generally less speculative, Hoos said.

“If they’re in the queue right now, they’re pretty mature and likely to come online,” she said.

New York must deploy new energy storage resources at scale to zero out power-sector emissions by 2040, as required by state law, Hoos said. By then, Aurora’s “merchant base case” scenario envisions 30 GW of flexible resources — including batteries and thermal peaking resources — supplying New York’s grid alongside 17 GW of offshore wind capacity.

A slower-than-expected ramp for the offshore wind industry may require heavier state support for longer-duration energy storage resources to meet the state’s storage goals, Hoos said. But even in a scenario where offshore wind development continues apace, its comparatively steady generation profile — with lower intraday volatility — makes the case for merchant energy storage less appealing than in solar-saturated markets like California and Texas, necessitating continued reliance on capacity markets and state offtake through the competitive Index Storage Credit mechanism, she added.

Nevertheless, “many of the developers we work with are starting to believe there’s a merchant or uncontracted case [for battery storage] downstate in the next couple of years … especially with less transmission being built between upstate and downstate,” Hoos said.

In December, New York and members of a public-private joint venture mutually agreed to cancel their contract for a 175-mile transmission line slated to bring nearly 5 GW of zero-emissions power into New York City by 2027.

At the same time, storage developers are pursuing “more creative solutions” for utility-scale storage deployments, like Arclight’s planned 15 MW/60 MWh battery installation replacing a retiring thermal unit at the Arthur Kill power plant on Staten Island, Hoos said.

“They have to build something, and they’ve said they don’t want it to be gas,” she said.

Article top image credit: Young777 via Getty Images

‘Interconnection processes must evolve’ to handle DER influx: DOE

The DER roadmap issued in the last days of the Biden administration envisions interconnection wait times under one day for <50-kW systems and 25% shorter power outage durations by 2030.

By: Brian Martucci• Published Jan. 24, 2025

To unlock the full potential of distributed energy resources in the next five to 10 years, utilities and grid operators must improve DER interconnection processes by increasing data access, streamlining study workflows and revising cost allocation approaches, according to a Jan. 16 report from the U.S. Department of Energy’s Interconnection Innovation e-Xchange, or i2X.

DER interconnection challenges are compounded by “significantly different resource availability, technology capabilities and grid impacts” for different technologies, such as wind, solar, small hydropower and energy storage, i2X said in its Distributed Energy Resource Interconnection Roadmap.

“Interconnection delays can definitely be a huge impediment for DERs, especially on the nonresidential side … [and] can also be a big reason why developers choose to exit certain states even with seemingly good economic opportunities,” said Hanna Nuttall, a U.S. distributed storage research analyst with Wood Mackenzie.

From 2010 and 2023, the number of U.S. residential rooftop solar PV systems rose from 89,000 to 4.7 million as the capacity of community solar installations grew from 1 GW to 7 GW, according to the i2X road map. Globally, energy storage capacity is expected to quadruple from 2018 to 2030, driven in large part by electric vehicles and related equipment, i2X said.

At the same time, interconnection waits are lengthening, even for relatively small DERs. In California, for example, the median interconnection wait for systems between 50 kW and 100 kW increased from about 60 days in 2010 to 100 days in 2022, i2X said.

“This is really a problem that can plague systems of any size,” Nuttall said. “Anecdotally, you could have a 100-kW solar system stuck in the queue for years.”

The i2X road map defines DERs as systems that meet three criteria:

Interconnected to distribution and sub-transmission systems not under Federal Energy Regulatory Commission jurisdiction;

Sized from “small behind-the-meter, kW-scale systems to larger, in-front-of-the-meter systems less than 80 MW,” and,

Technologies subject to interconnection study, such as wind, solar PV, small hydropower and energy storage, but generally not demand response or electric vehicles.

The i2X grouped its recommendations for improved DER interconnection processes into four broad groups: enhancing interconnection studies through “more transparent and accessible data sharing and strategic use of automation;” streamlining the interconnection process to reduce bottlenecks; promoting economic efficiency in interconnection to reduce costs to ratepayers; and addressing the performance of inverter-based DERs to maintain and enhance grid reliability and security.

“DOE put forth some really good recommendations here, some of which some utilities [already] do to a certain extent,” Nuttall said.

Those include publishing hosting capacity maps that improve DER developers’ and owners’ access to grid data; moving toward flexible interconnection practices that weigh the economic impact of unscheduled congestion-related curtailments against grid upgrade costs borne by developers; setting standard interconnection timelines; and reforming the “cost-causer pays” model to spread costs for interconnection-related upgrades among a wider group of beneficiaries, Nuttall said.

“We really need a lot of innovation to get DERs onto the system,” especially on more congested grids like ISO New England’s, she said.

The i2X road map set five targets to track progress on DER interconnection reform: shorter interconnection times; higher interconnection completion rates; better availability of interconnection data; no “[bulk power grid] disturbance events exacerbated by inaccurate DER modeling;” and faster service restorations after power outages.

By 2030, the road map aims for median interconnection times of one day or less and completion rates greater than 99% for systems smaller than 50 kW, under 75 days and greater than 90% for systems between 50 kW and 5 MW, and under 140 days and greater than 85% for systems 5 MW or larger. Additionally, it targets a 25% reduction in average outage duration and envisions “public, detailed and current queue data” available for all U.S. states and territories.

Article top image credit: aydinmutlu via Getty Images

Sponsored

A glimpse of the future of distributed energy resources

Where do today’s load management activities - including demand response, energy efficiency, and renewable energy programs - fit in a distributed energy resource (DER) future of non-wires alternatives, storage and more? A recent publication titled “The Future of Distributed Energy Resources: A PLMA Practitioner PerspectivesTM Compendium” details eight industry initiatives where leading utilities are partnering with their customers and allies to demonstrate the path to a more integrated approach to DERs.

Peak Load Management Alliance (PLMA) members, utility companies, consultants, and vendors have deep experience in delivering practical solutions to the operational requirement to balance resources and loads. And while the first 100 years of the energy industry was focused on matching resources (generation) to loads, the next several decades will be focused on flexible loads efficiently meeting generation output at both the Transmission system and Distribution feeder level, incorporating renewable, distributed and intermittent resources. We are moving into the realm of dynamic management of the system every day. The last decade has seen a rapid increase in behind-the-meter solar installations; recent advances in battery and thermal storage, electric vehicle (EV) charging, and load flexibility resources are also indicators of the growing importance of distributed energy resources (DERs).

The PLMA community has a history of sharing experiences that enable others in the industry to understand, learn, and embrace industry change. In keeping with this mission, PLMA asked its membership to share case studies about current DER activities and projects. The initiatives detailed in the Compendium are:

Planning/Foundational Category – Defined as those utilities taking bold steps to leapfrog pilots/technology straight to integrative planning and procuring, and change management.

Hawaiian Electric’s Integrated Grid Planning,Hawaiian Electric Company

Distributed Resource & Flexible Load Study,Portland General Electric and Navigant

Integrating DER Planning,Research and Program Development, Tacoma Power

“DR Plus” Category – Defined as customer-sited assets (with or without the involvement of an aggregator) to monetize DER operations for utility/grid benefits to a growing spectrum of network problems.

Deriving New Wholesale Market Revenue Opportunities and Maximizing Customer Utility Savings with Behind-the-Meter Distributed Energy Resources,Center for Sustainable Energy, Tesla, Conectric Networks, and Olivine

Expanding National Grid’s ConnectedSolutions Program to Include Energy Storage,Sunrun, EnergyHub, and National Grid

Microgrids Category – Defined as customer-sited assets that have great degrees of flexibility and opportunity for monetization.

Microgrid Enables Military Facility to Participate in Utility Services,Eaton

Energy Storage and Microgrid Performance in Non-Wires Solutions and Other Demand Management Programs,Enel X

International Category

First Movers in DER in Colombia,U.S. Energy Association

If management is asking “where do today’s load management activities (including DR, EE, and renewable energy programs) fit in a distributed energy resource (DER) future?” the eight case studies in the Compendium offer a glimpse into the future that is unfolding today. If imitation is the sincerest form of flattery, then now is the time to embrace progress through plagiarism. Here, PLMA members provide the blueprints for utilities, regulators and service providers to follow. Read the Compendium at www.peakload.org/plma-publishes-future-of-der-compendium.

Article top image credit:

AI improvements, DERs and new generation needed to meet power demand: USEA panel

“Serving data center load is absolutely a national security challenge,” said NERC President and CEO Jim Robb.

By: Robert Walton• Published Jan. 22, 2025

The long lead time to build newdispatchable generation has electric utilities scouring their distribution systems for available electrons — but ultimately, new gas and nuclear resources will be required to meet skyrocketing demand, experts said Jan. 15 during a U.S. Energy Association discussion.

A combination of data centers, manufacturing and electrification is driving U.S. electricity consumption higher after two decades of stagnant growth. Demand is projected to grow 9% by 2028 and 18% by 2033 — an increase of 2% per year, on average, relative to 2024 levels — consulting firm ICF said in a September report. Peak demand could grow 5% over the next four years.

What must utilities do in order to meet the coming demand?

“Build everything you can, as fast as you can,” said Duane Highley, CEO of Tri-State Generation and Transmission Association.

“The supply chains are lengthening. To get a turbine on order might be 2030, 2031, delivery. We’re going to need some gas in the mix to make it all happen, even as we build massive amounts of renewables. So I’d say just move as fast as you can today,” he said.

“We have to definitely build more, but we also have to expand the capacity of the existing systems that we have,” said Karen Wayland, CEO of GridWise Alliance, a group focused on electric system innovation.

Distribution utilities facing significant load growth will likely need new and expanded transmission capacity and generation, but those projects will lag the new load, Wayland said. “So many utilities ... are looking much more closely at local resources.”

The California Independent System operator “counts those resources towards overall West-wide reliability,” she said. But along with distribution resources, the sector will need to “build much more generation at scale that we haven’t seen, in particular nuclear as well as natural gas.”

“In the last three year we generated and processed more data than we have in all of history, and we’re looking in 2025 at 200 zettabytes of data,” Pope said. A zettabyte is equal to a trillion gigabytes.

But stakeholders say there are reasons to believe the utility sector can meet the coming demand.

“The hyperscalers, as well as tech companies, are really looking at how they make energy consumption in their algorithms and in their chip design much more efficient,” Pope said. And EPRI and other stakeholders are working on peak load management approaches, allowing data centers “to flex within the system.”

Improvements to AI algorithms are already happening and will continue, said Sacha Fontaine, principal utility consultant and AI expert for SAS.

“We have focused on the efficiency of the computation,” Fontaine said. “Our computation engine from 18 months ago is 30 times as efficient. So there is a shift of focus.”

But the electric sector must see near-term challenges as an emergency situation, said Jim Robb, president and CEO of the North American Electric Reliability Corp. The reliability watchdog has for years been warning that retiring baseload generation was being replaced by intermittent resources, creating resource adequacy concerns.

Load growth forecasts have tripled in the last three years, Robb said.

“Serving data center load is absolutely a national security challenge for the country and it’s going to stress our resource adequacy situation,” Robb said.

“We’ve got to figure out how to build new generation. We’ve got to figure out how to build long distance transmission. And those projects don’t happen quickly,” Robb said. “So we’ve got to start working on this problem yesterday.”

Article top image credit: Andrey Semenov via Getty Images

Texas task force aims to ‘tear down barriers’ to virtual power plant pilot as participation lags

The aggregated DER pilot, which includes Tesla and Bandera Electric as participants, aims to harness 80 MW of flexible resources on the Texas grid, but it has not reached that goal.

By: Robert Walton• Published Dec. 11, 2024

The Electric Reliability Council of Texas is considering doubling the size of a virtual power plant pilot project, in addition to making a slate of other changes aimed at growing the underutilized program.

The aggregated distributed energy resource pilot, or ADER, launched in 2022 with a goal to harness 80 MW of flexible resources, primarily batteries, on the ERCOT grid. But so far only Tesla and Bandera Electric Cooperative have brought aggregations to the grid, accounting for about 15 MW.

The ADER project aims to evaluate the participation of aggregated distributed resources in the ERCOT wholesale market, but experts say initial limits on the program have kept it from achieving its goals.

Commissioner Jimmy Glotfelty has helped lead the ADER effort from the Public Utility Commission of Texas, working as a liaison to the task force which developed the initial rules for the pilot project with the grid operator.

“I’m happy with where we are,” Glotfelty told Utility Dive. “But there are some things which need to change” about how the program is set up. “Success, to me, is if in three years, or two years, we have 300 MW or 500 MW and it’s a general part of the market system.”

At a time when Texas energy demand is rising and the state is rushing to add resources, lawmakers have taken an interest in the ADER program and how it can help keep the state’s electric grid reliable.

ERCOT Senior Vice President and Chief Operating Officer Woody Rickerson testified before the Texas Senate Committee on Business and Commerce in October, discussing challenges which have limited the ADER program. Whereas the grid operator has typically focused on larger, transmission-connected resources that might be 100 MW in size or larger, ADER focuses on pulling together resources around 0.1 MW in size, operating at lower voltages.

“That’s not something ERCOT has typically had any hand in,” Rickerson said.

“It sounds like a lot of work to get 15 MW,” said Sen. Charles Schwertner, a Republican and chair of the Senate Committee on Business and Commerce.

“It has been a lot of work, but I do think it has some potential,” Rickerson replied.

Difficulty in getting DER aggregations to respond to precise grid signals has been one barrier to their participation in the ERCOT market. “We’re opening up a new phase where there will be bigger signals so [aggregations] won’t have to be as precise,” Rickerson said.

There are also potential changes to how qualified scheduling entities, or QSEs, represent aggregations in the market. In ERCOT, QSE’s submit bids and offers to ERCOT on behalf of resource entities or load serving entities, charging fees for their service. And ERCOT does not allow aggregators to bundle aggregations across load zones, further raising costs for aggregators.

“That is the number one barrier to entry” to ADER participation, said Arushi Sharma Frank, founder of energy consulting firm Luminary Strategies. Sharma Frank participates on the Public Utility Commission of Texas’ ADER task force through her company, and formerly served as vice chair when she worked for Tesla.

While large, centralized generators have revenue potentials that are much larger than the cost of telemetry systems and other QSE costs, ADERs have a break-even point around 15 MW to 20 MW, Sharma Frank wrote on behalf of Tesla in 2023 in a task force memo. “This scale is at or above current QSE caps, which must be increased,” she wrote, referring to the ADER pilot’s initial limits.

Sharma Frank says a host of barriers to entry have limited the ADER pilot’s size.

“We were far too conservative on Day One of the pilot because it was new,” she said. The 80 MW cap was too low, and it was split across eight settlement zones creating multiple smaller caps. Other limits — such as what services the pilot could provide to the ERCOT market — have also kept the program from fulfilling its potential, she said.

The caps and limits “create a depressing signal on market interest,” Sharma Frank said. “You can’t create a model of what you could get out of a program at its zenith, if what the regulators give you up front is a bare fraction of that, and there’s no certainty of opportunity.”

The commercial and strategic work required to pull off complex, multi-party relationships in the ERCOT market, like the ADER pilot, “fundamentally rests on there being such a huge number on the other side, of value, that all these folks can come in and sit at the same table and agree to split that value,” Sharma Frank said. “That’s the opportunity that was missing.”

Glotfelty has also pressed for consumers to be able to register their equipment with the aggregator of their choosing. In particular, he has expressed concern that Tesla Powerwalls are only able to participate in the ADER project through a Tesla retail provider.

“We have an open market in Texas, and choosing how you want to be a part of a resource group should be part of that,” he said.

The task force is hoping to address many of the barriers with an update to the pilot’s governing documents. ERCOT has just completed a first pass of those changes and sent red lines of the governing documents back to the group. Those changes will be reviewed at a Dec. 18 meeting.

If the task force agrees with ERCOT’s changes, then the grid operator will complete a final review and the changes go to the commission for approval. The first quarter of next year seems to be the “right guess” for when that will happen, Sharma Frank said. She expects the market can respond to the ADER updates within a year because so much time has already been spent addressing technical issues.

The changes

The first and second phases of the ADER pilot limited the combined registered capacity of all ADERs to 80 MW and subsequently split the services they could provide, 40 MW each between ERCOT’s ancillary non-spin and contingency reserve services. The grid operator is now proposing to increase those limits to 160 MW and 80 MW, respectively, “to allow the pilot to continue to grow and evolve,” according to task force workshop documents from the Nov. 18 meeting.

The proposed changes also include allowing aggregations to participate in the ADER project through a new Aggregated Non-Controllable Load Resource framework, or A-NCLR, which will accommodate more “blocky” responses from aggregations struggling to meet telemetry requirements.

“Blocky” refers to larger loads coming off the system in chunks, as opposed to smaller amounts of capacity.

NCLRs are typically large demand response resources on the ERCOT system that respond in bigger chunks than the 5-minute granular responses the ADER pilot initially required from devices.

“Some of the technical requirements for participation in some of the ancillary services are a little onerous,” Glotfelty said. “And they are onerous for a reason — to ensure that we could, in this first phase, aggregate different amounts of load across regions, and that we could find ways to ensure that the market signals and the pricing was set accurately.”

Now the task force is looking for ways to “tear down barriers” to resource participation, he said.

“The A-NCLR framework makes both communication to and from an aggregation of devices, and the response, easier and cheaper for the participants to provide, and more blocky in how ERCOT views it, which is just an extension of how ERCOT already receives blocky responses from large loads today,” Sharma Frank said.

The proposal also opens the door to bundling aggregations, Sharma Frank said.

“Because the response is blocky, the technical back-end work that one QSE has to do should decline sharply, and we should be able to take multiple entities’ aggregations through a single chain of command to ERCOT,” Sharma Frank said. “It would completely change the barrier-to-entry problem.”

As for issues of interoperability, and moving equipment from different manufacturers between aggregators, Sharma Frank expects those issues will be addressed as the market expands.

“The interoperability challenge in Texas is related to ... the suppression of economic growth value,” she said. Equipment manufacturers are not going to spend money to integrate with new providers if the revenue opportunity is small, she said.

Beyond batteries

The future of DER aggregations in Texas will hinge on the effective integration of resources and expanding what types of resources can be aggregated, John Padalino, chief administrative officer and general counsel of Bandera Electric Cooperative, told the Senate Business and Commerce committee. Bandera is one of the two ADER aggregations operating today, along with Tesla.

In 2017, Bandera developed Apolloware, an appliance-level electric meter that can provide real-time energy feedback, Padalino said. It can connect devices from different manufacturers while also meeting ERCOT’s telemetry requirements.

While a limited number Texas homes have battery backup systems, Padalino said about 1.3 million do have smart thermostats. “If we convert just 40,000 thermostats into registered ADER participants, we can achieve the 80 MW goal,” he told lawmakers.

For now, the ADER program is largely designed to accommodate small devices capable of dispatchable exports of energy to the system, Sharma Frank said. But the changes to allow for blockier load participation could mean more types of devices are enrolled.

NRG and Renew Home announced last month they are partnering to deploy hundreds of thousands of smart thermostats across Texas to support a residential virtual power plant with nearly 1 GW of capacity by 2035. The VPP is not a part of the ADER project but “speaks to a large-scale effort to increase our VPP capabilities in ERCOT,” NRG said in a statement.

Reliant, NRG’s flagship retail electric provider in Texas, has an aggregation that is registered with the ADER pilot and is undergoing testing with ERCOT, the company said.

Sharma Frank said NRG’s announcement is “a follow on to the fact that ADER has created a roadmap for revenue certainty.”

“No one entity had ever successfully put out lots of megawatts from an aggregation of sub 1-MW sites. Now that we’re actually doing it, ERCOT is learning a lot from that process and they’re creating validation around the technology,” Sharma Frank said. “It has made the market opportunity more meaningful, scalable and more certain, because it’s actually happening.

Article top image credit: Cavan Images via Getty Images

When TOU rates aren’t enough: BGE, other utilities expand active managed charging for rising EV load

Time-of-use rates work, but the resulting snapback peaks necessitate additional measures to prevent distribution system overload.

By: Herman K. Trabish• Published Dec. 4, 2024

Transportation electrification, if not effectively managed, may become the most disruptive new electricity demand on the power system, analysts and utility leaders agree.

Electric vehicle drivers prefer home charging for its low cost and convenience despite the longer charging times, according to a 2023 study by the National Renewable Energy Laboratory. But to keep pace with the growth of EV charging and other customer needs, as of 2021, “utility investments in distribution systems, nationwide, exceeded $60 billion annually,” a 2024 study by NREL found.

That investment is needed to “optimize, visualize and control” new distribution system resources, Pacific Gas and Electric CEO Patti Poppe acknowledged during the RE+ 2024 clean energy conference in September. But revenues from new electricity sales will “offset the infrastructure investment” and “reduce all customers’ bills between 2% and 3%,” she stressed.

And using active managed charging instead of time of use rates to shift charging to the lowest electricity price periods could save another $300 per vehicle per year, according to a just released Smart Electric Power Alliance paper.

“It is becoming clear time of use rates are not enough” and “are creating secondary peaks that cause distribution system congestion,” said report co-author and SEPA Senior Analyst, Research and Industry, Brittany Blair. “Active managed charging” by utilities and third parties “will be needed to unlock EVs’ full potential and decrease distribution system impacts,” she added.

Pilot programs have proven active managed charging is effective and utilities in Maryland and other states are moving programs to scale. But key questions remain about whether state regulators and stakeholders will see the value proposition in distribution system modernization investments and what it will take to get customers to give utilities and third parties control of their charging.

Permission granted by EEI

The snapback peak problem

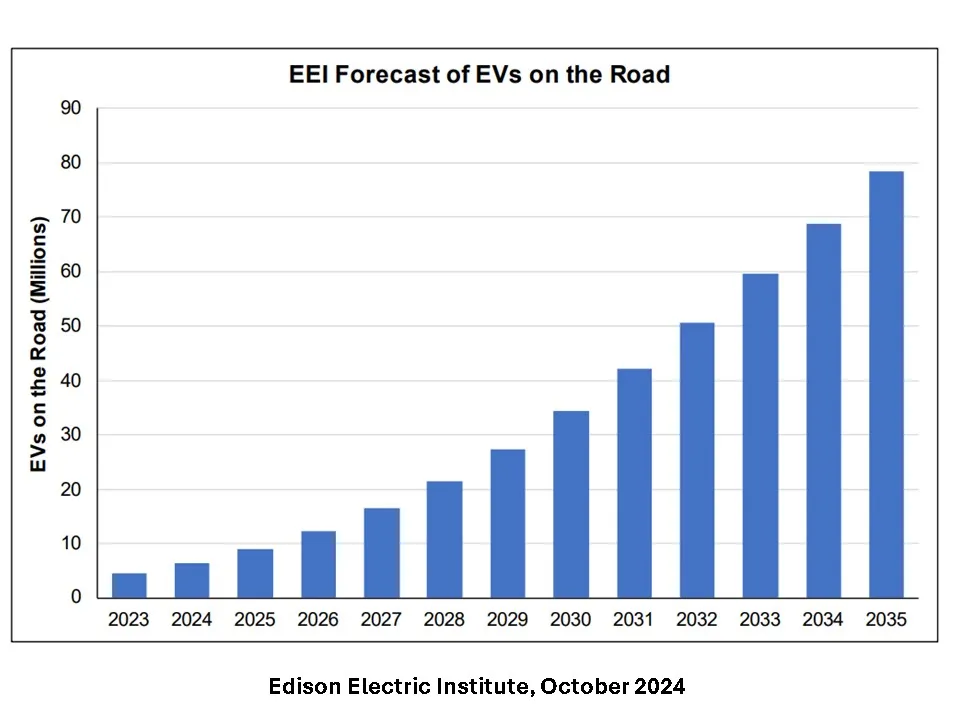

There could be 78.5 million EVs on U.S. roads by 2035, up from 2023’s 4.5 million EVs, according to an October 2024 paper from investor-owned utility trade association Edison Electric Institute.

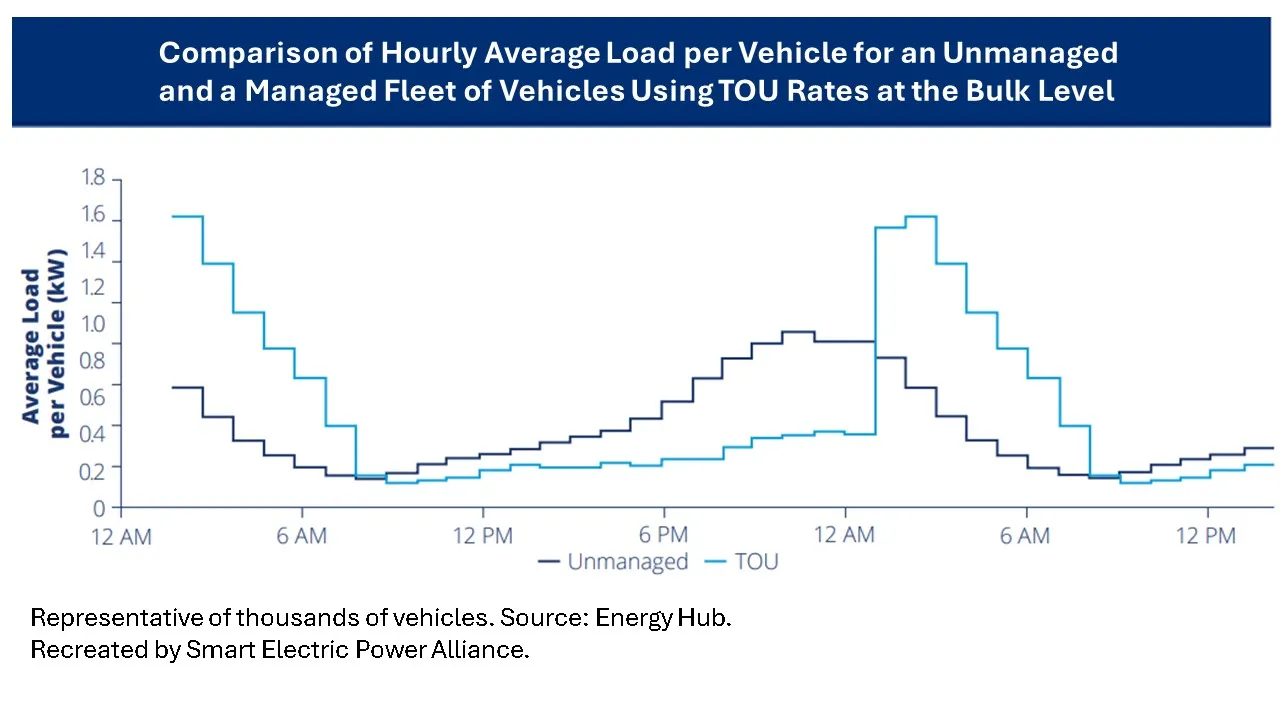

While TOU rates shift residential and business electricity use away from peak demand periods, they are less effective for managing EV charging, a just-released Electric Power Research Institute paper concludes. Charging is too often initiated immediately after the reduced rates begin, causing what many call a secondary, or snapback, peak, the research confirmed.

TOU rates “are definitely helpful” because they limit the system burden “at the primary peak,” said Southern California Edison Director, Clean Energy and Demand Response, Chanel Parson. But there is a secondary peak right after the peak period ends, she acknowledged.

That secondary peak can be managed “to come on gradually” if the utility is allowed to “orchestrate the flexible load to prevent localized distribution system congestion,” Parson said. Active utility managed charging can spread charging over the TOU off-peak period if there are “incentives for customers to participate, either from the utility or third-party aggregators,” she added.

A way “to stage distribution system investment with the growth of EVs” may be in using new accelerated computing capabilities to deliver electricity market price information to local substations, said Kay Aikin, founder and chief product officer of consultant Dynamic Grid. Though not widely tested, that “substation intelligence” could manage charging with “price signals to EV chargers pre-set to owner parameters, eliminating direct utility control,” she added.

Another approach is the smart panel, which is an energy management system that sheds EV charging if it threatens to overload the home’s rated service, said SPAN Director, Homebuilder Services, Stephen Kane.

But if several houses in a neighborhood are charging EVs, the total load could still be an issue at the feeder or transformer, he acknowledged. “The utility has to be responsible for load at the system level,” Kane said.

The proven solution is active management of charging by the utility or a third party, many stakeholders now realize.

Permission granted by SEPA

The active managed charging solution

With over three million EVs on U.S. roads, managed charging pilots need to be scaled before infrastructure upgrade costs start rising instead, analysts and utility executives agree.

As documented in the SEPA paper, “utilities have done enough active managed charging pilots to understand its value and its effectiveness,” said SEPA’s Blair.

And utilities do not need total control of EV charging, said SEPA Senior Director, Electrification, and paper co-author Garrett Fitzgerald. Many utilities are beginning to understand that third party aggregators with DER management systems at the distribution system level can effectively implement signals from utility control rooms, he said.

An Arizona Salt River Project 2021 study, the Pacific Gas and Electric ChargeForward California program, and National Grid’s Charge Smart plan in New York are examples of such utility progress, according to the SEPA paper.

“The majority of the value that we are quantifying and designing customer compensation around are from system-wide peak energy cost reductions,” Fitzgerald said. But “each customer will have a different value, and managed charging can be optimized to focus on those customers where a shift in charging is needed, rather than on shifting all customers.”

Utilities recognize they can minimize the cost and maximize the benefit of EV charging with active management to put downward pressure on rates and improve system reliability for all customers, agreed EEI Senior Director of Electric Transportation Kellen Schefter.

A January 2024 Synapse Energy Economics study showed “revenues have exceeded the costs of managed charging programs” and offers guidance on “the art of program design,” Schefter continued. “A program design that will change an individual customer’s behavior may also require a TOU rate, an upfront bill credit for enrolling, or an ongoing monthly or annual incentive to continue to participate,” he said.

EV advocacy consortium ChargeScape found very different incentives in the Duke Energy Carolinas EV Complete Home Charging Plan and the Xcel Energy Colorado Charging Perks Pilot got good participation, Schefter said.

“Solutions that meet different customer needs and offer different options will likely be needed,” Schefter added. But “programs can now cost-effectively scale,” and Baltimore Gas and Electric, or BGE, is demonstrating that with its just approved plan to serve up to 30,000 EV owners, he said.

“EV charging load is a major concern of almost every major utility now because even where EV adoption is not high, some high adoption neighborhoods may exceed local system capacity,” Leach continued. WeaveGrid uses BGE electricity pricing and system demand information to optimize charging at the grid edge, according to EV owner pre-set preferences, she added.

“We are still working on the benefit-cost analysis by modeling the cost of distribution system upgrades with and without managed charging,” Leach added.

The costs of serving the current and coming EV charging demand will likely be high, analysts generally agree.

But there will also be significant costs for building out the distribution system to enable active managed charging, stakeholders acknowledged.

Permission granted by SEPA

Managing managed charging

Grid modernization regulatory proceedings and rate cases have shown the potential upward rate pressure from the costs to implement and deploy managed EV charging programs and technologies.

SCE “is developing a large-scale managed charging program that will include a TOU rate, an upfront cash incentive, and other incentives to cover the cost of equipment, Parson said. And an estimated 80%-plus electricity demand growth to meet California’s 2045 net zero emissions goal will require utility DERMS, system-wide hardware and software, and grid edge technologies,” she added.

To avoid imposing costs on non-EV owners, SCE is considering “grant funding and industry partnerships,” Parson said.

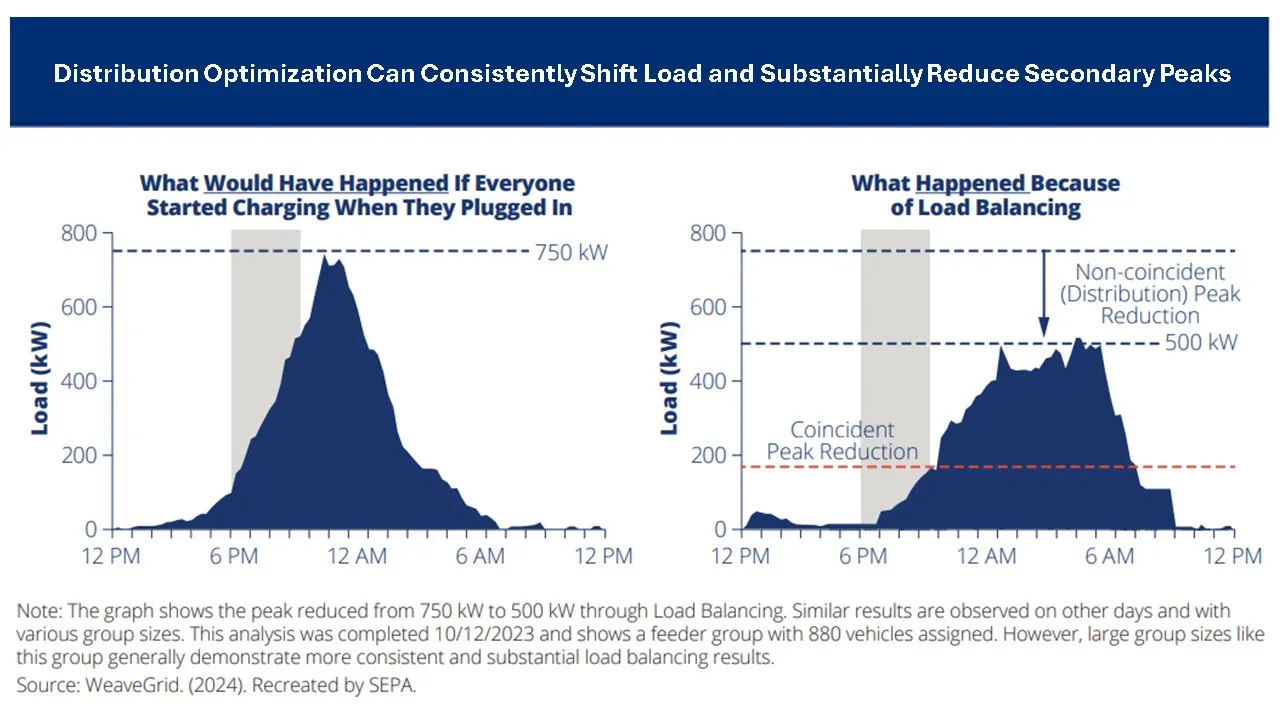

The BGE SCM pilot will scale to enroll 30,000 EV owners by 2027, but it will delay or minimize distribution system capital investments for handling EV charging loads, said WeaveGrid VP of Market Development Mathias Bell. WeaveGrid’s EV management system and customer facing DERMS reduces the need for utility investments at the grid edge, Bell said.

“The pilot demonstrated a cost-effectiveness of 1.58 under the required Maryland jurisdiction-specific test, showing a benefit greater than the program’s cost,” Bell said. And “92% of the charging load managed through SCM complied with the charging schedule set by BGE and WeaveGrid,” he added.

WeaveGrid is also working on active EV charging management with Oregon’s Portland General Electric, California’s Pacific Gas and Electric, Colorado’s Xcel Energy, Detroit’s DTE, and Southern Company’s Georgia Power and Alabama Power subsidiaries, Bell said.

Active managed charging is ready to scale, agreed Senior Vice President, Head of Customer Solutions, Erika Diamond of grid-edge DERMs provider EnergyHub.

“There is complexity in managing charging” because utility control rooms expect both “effective load shifting and consumer satisfaction,” Diamond said. But a complete utility control-room DERMS takes time to design and implement, while “a grid-edge DERMS can be deployed as quickly as in weeks,” which is why utility aggregator partnerships are growing, she added.

Adding DERMs to a utility control room can take six to nine months, Schneider Electric Digital Grid Product Marketing Manager Monika Jovic confirmed in a July webinar. And grid edge DERMS deployed and managed by third party aggregators can manage flexible distributed resources like EV charging “to replace traditional resources,” Jovic said.

EnergyHub “has programs involving over 100,000 devices” and “is working with utility planning, operations and demand-side management teams,” Diamond said. Its grid edge DERMs integrates utility control room information with its situational awareness at the distribution system level “to balance supply and demand to match the load shape,” she added.

“Most utilities and aggregators have not yet quantified the full range” of energy, capacity and ancillary services values of managed charging beyond peak reduction, Diamond continued. Determining that full value may “require the value paradigm of distributed resources to evolve,” she said.

Correction: A previous version of this story gave an inaccurate acronym for Baltimore Gas & Electric. It goes by BGE.

Article top image credit: Courtesy of General Motors

EPRI, Kraken advance DER interoperability standards to boost virtual power plant deployment

“Without interoperability standards, VPPs cannot reach scalability, affordability, and reliability as soon or as efficiently as they will be needed,” said EPRI CEO Arshad Mansoor.

By: Herman K. Trabish• Published Nov. 27, 2024

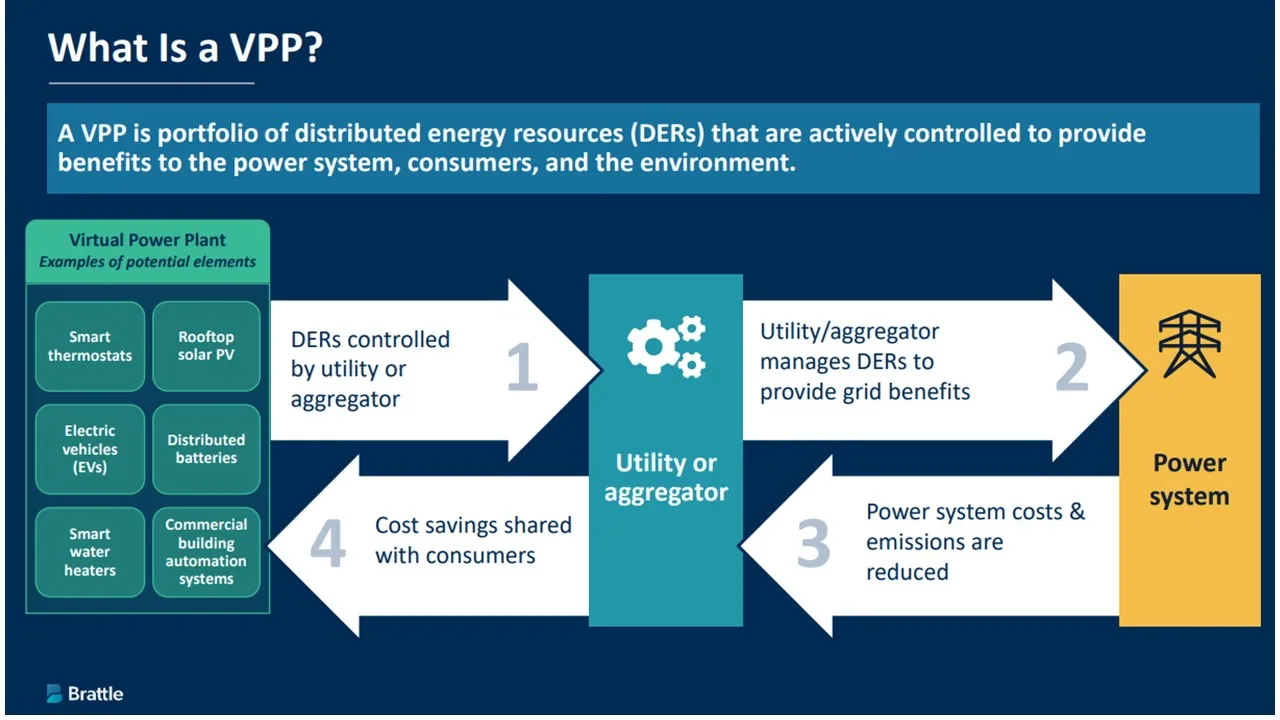

The growth of virtual power plants, which are large portfolios of consumer-owned distributed resources, is about to get a big boost.

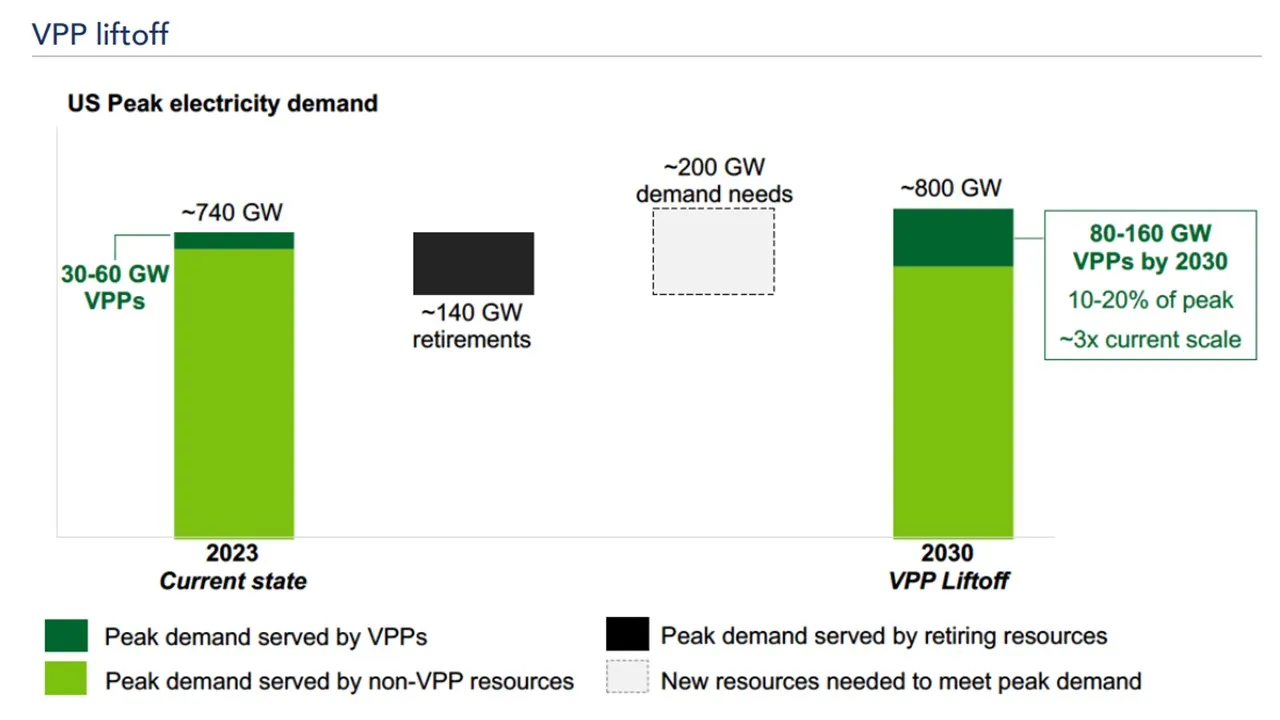

VPPs could meet as much as 160 GW of the 200 GW of U.S. peak demand needs in 2030, and reduce power system costs by $10 billion annually, according to a 2023 report from the Department of Energy. But VPP growth could be limited by the lack of common standards in their aggregated distributed energy resource components, developers and advocates say.

Common standards allow utilities or aggregators to “orchestrate” diverse DER like rooftop solar, batteries and electric vehicles in a full range of power system services, proponents say.

“Without interoperability standards, VPPs cannot reach scalability, affordability, and reliability as soon or as efficiently as they will be needed” to meet the coming variability, growing load and extreme weather events the power system faces, said Arshad Mansoor, CEO of the Electric Power Research Institute, which is leading two standardization initiatives. “Now is the time to bring VPP stakeholders together,” he added.

Standardized interoperability can help simplify and expand the needed adoption of DER and the needed integration of VPPs into utility planning and wholesale markets, the DOE report said.

System operators “must have visibility of connected DER devices, be able to signal the devices, and be confident they responded to the signal,” said Lon Huber, senior vice president, pricing and customer solutions, with Duke Energy. For that, “the entire VPP ecosystem should be standardized by a multi-stakeholder collaborative,” he added.

The big unanswered questions advocates are now confronting, however, are what the standards should be and what technologies will be needed to optimize performance. EPRI, international software platform provider Kraken and others are joining to acknowledge and answer these questions.

Flexibility becomes vital

Transportation, building and industrial electrification will lead to new electricity demand dynamics, including higher and more time-varying demand spikes, analysts agree.

VPPs can make automatic small shifts in customer energy use to “when electricity is cheaper and cleaner,” said Ben Brown, CEO of Renew Home, which operates 3 GW of VPPs and is targeting 50 GW by 2030. “Demand flexibility across thousands of homes” is “a significant peak capacity resource” and “helps balance power system supply and demand,” he added.

VPPs are “likely the only way” to manage electrification “at a reasonable cost and on the timeline we need,” DOE Loan Programs Office Director Jigar Shah said in a recent interview.

With the enormous growth of electricity load, the flexibility of VPPs “is the only way to match demand and supply,” agreed Sunrun Head of Grid Services and VPPs Chris Rauscher. Demand from electrification will grow but VPPs “will consistently bring down the peak,” and “create incremental capacity” on the power system, he added.

VPP flexibility has also strenghtened resource adequacy in California and Arizona, relieved stress on transmission and distribution systems in New York, and reduced system costs for customers in Utah and Vermont, according to a September Rocky Mountain Institute report.

But “fully realizing” VPP flexibility will require full integration of VPPs into power system planning and operations, the report said. And device standards to ensure more consistent, reliable dispatch — and more accurate and timely dispatch signals are “critical” to VPP integration — it added.

The “potential $10 trillion” cost to upgrade the U.S. distribution system to meet current electrification goals can also be avoided by “a system that rewards flexibility,” said Kay Aikin, CEO of distribution level software solutions provider Introspective Systems.

Using flexible VPPs allows “staged distribution system investment” as load grows, Aikin said. “Many utilities are beginning to see VPPs relieve system congestion, and their interest in flexibility is growing,” she added.

A key step toward flexibility is DER interoperability standards, EPRI and other advocates say.

Permission granted by Brattle Group

Standards to meet complexity

The aggregation of customer-owned devices at the distribution system level introduces a new complexity into power system and market operations, industry stakeholders agree.

Many, even in the electric power industry, do not realize how limited visibility into the distribution system is in today’s legacy distribution system, said Association of Edison Illuminating Companies Vice President, Technical Strategy, Elizabeth Cook. “Regulators and policymakers need to allow utility investments in foundational distribution system sensor and measuring technologies,” she added.

The communications technologies and software platforms now being used “are not dynamic enough” to capture the potential benefits of today’s dynamic DER technologies, Cook continued. But obtaining the needed distribution system baseline information and modeling data will require “a systematic overhaul” of technology and operations, she said.

To advance the overhaul, and enable VPPs to provide system flexibility and reliability, EPRI and Kraken are launching their Mercury initiative to develop interoperability guidelines and practices for DER, said Kraken Chief Marketing and Flexibility Officer Devrim Celal. The initiative will begin by developing a leadership group of VPP stakeholders, Celal said.

Like the Bluetooth Special Interest Group that was founded in 1998 and developed wireless device standards, VPP stakeholders will identify DER communications protocols, Celal said. The greater visibility and more accurate control of the component devices “will enable VPPs to better balance loads, reduce system congestion, and interact with wholesale markets,” he added.

An effort will follow to bring an even wider range of VPP stakeholders into EPRI’s Flexible Interoperable Technologies, or FLEXIT, initiative. The initative’s objective is to go beyond Mercury by simplifying DER integration “through standardizing service definitions and interfaces; and to develop a future-proof implementation strategy,” EPRI said.

“Diverse stakeholders including utilities, DER manufacturers, VPP aggregators, researchers, and government agencies, will help develop a public VPP aggregation and technical framework for a utility-to-aggregator interface,” EPRI’s Mansoor added.

Because current VPP-utility interfaces are unique to each aggregator or utility, VPP integration requires costly “custom software” and “months or years” to complete and implement, Mansoor said. “In the worst cases, the effort required outweighs the benefits,” but standardization and interoperability can change that, he added.

DOE. (2023). “VPP Liftoff paper” [pdf]. Retrieved from DOE.

“VPPs are built and used now, but they will not be scalable, reliable, and affordable without standardization and interoperability,” Mansoor continued. “VPP flexibility will still be valuable as energy, capacity, and ancillary services, but manufacturers will not invest in enabling VPP products, and the value will not be fully integrated into markets,” he said.

Key stakeholders agree.

With multiple technologies working together, VPP deployment “can scale to serious numbers,” said Duke’s Huber. Standardization through “a multi-stakeholder collaboration” will allow the needed system visibility, controls and communications for “device discovery, device enrollment, device orchestration, and device data exchange” in VPPs at scale, he said.

Another effort to streamline VPP deployment is a model tariff designed by law firm Keyes and Fox for Solar United Neighbors “to set compensation at the full value of the service,” said Keyes and Fox Partner Beren Argetsinger. They also designed model legislation to expand VPPs into new jurisdictions, he added.

Further DER standardization is not necessary for Sunrun, which primarily provides residential solar-plus-storage VPPs that are already “operating at scale with reliability and predictability,” said Sunrun’s Rauscher. “Utility program administrators do, however, need to standardize software for automated notifications of the need for peak load reductions to aggregators and customers,” he added.

Other stakeholders see the need for more fully standardized interoperability among utilities, aggregators and DER technologies to enable VPPs to earn the full value they can provide.

Permission granted by Brattle Group

From standards to value

More value will come as VPPs expand from residential solar and storage to the full range of smart customer-owned DER technologies with standardized interoperability, including electric vehicle chargers and smart thermostats and home appliances, aggregators and utilities said.

Currently, monetizing VPPs is largely limited to “the portion of value that doesn’t require advanced controls and communication,” said Brattle Group Principal Ryan Hledik. But “streamlined communications” allowing “improved interoperability” can make managing the “fragmented set of technologies and software packages” affordable, he added.

A grid edge distributed energy resources management system, or DERMS, can streamline communications, Hledik and other VPP advocates said.

A grid-edge DERMS is the middle layer between customer-owned devices and the dispatch of devices in response to utility signals, said Erika Diamond, senior vice president and head of customer solutions for DER aggregator EnergyHub. An aggregator’s software can make a VPP operational and cost-effective within months and relieves the utility of grid-edge complexities, she added.

A grid-edge DERMS can use aggregated DER “to replace traditional resources,” agreed Schneider Electric Digital Grid Product Marketing Manager Monika Jovic in a July webinar.

Different opinions among aggregators about the need for DERMS may depend on the DER components of a VPP.

Each utility wants to manage its distribution system resources differently, said Sunrun’s Rauscher. “Any utility in the country can have a VPP program today” using residential solar and storage because aggregators have already made the needed investment in independent software platforms, he added.

Sunrun can also manage DER other than solar and batteries and is integrating devices like smart thermostats and heat pumps, Rauscher continued. But “there is a cost for that,” and the longer-term revenue certainty does not justify the cost of integrating “with each individual utility software platform,” he added.

The Mercury and FlexIt initiatives are intended to establish interoperability standards that expand the range of potential VPP resources while returning value for the services they provided, other VPP stakeholders said.

“A solar and storage VPP may run without a DERMS, but a grid-edge DERMS could enable any DER device to be a grid asset,” Diamond said. “Utilities are adopting individual DER programs but don’t know how to value a program that can dispatch the many different customer-owned DER across the distribution system 24/7 to meet system needs,” she added.

The visibility provided by a DERMS gives operators a “surgical” ability to use the customer-owned DER at specific locations in specific ways to meet specific needs, agreed Brattle’s Hledik. “Coordinating and simplifying” supply and demand balancing may not, though, streamline the integration of VPP operations with the many utility tariffs and programs and diverse markets, he said.

But standardization and interoperability will enable utilities to affordably scale VPP products so that markets will value and respond to them, EPRI’s Mansoor said. And that will lead to market rules that can integrate those products, he added.

“The power system is likely to need a lot of flexible resources in the coming decade,” EnergyHub’s Diamond said. “It will take all the flexible resources that are available,” and the projected value of that flexibility is likely to make VPPs “totally scalable and affordable,” she added.

The Mercury Initiative launches Dec. 5, the FlexIT Initiative will follow early in 2025, and as key power sector stakeholders join, their input will determine the course of the initiatives’ development, EPRI’s Mansoor said.

Article top image credit: Sakorn Sukkasemsakorn via Getty Images

New Jersey proposes incentives for grid-connected, distributed energy storage

The New Jersey Storage Incentive Program could provide up to $400/kWh in initial benefits for eligible behind-the-meter storage systems, the public utility board said Nov. 12.

By: Brian Martucci• Published Nov. 19, 2024

New Jersey is proposing upfront and performance-based financial incentives for grid-connected and behind-the-meter energy storage systems beginning next year, the state’s public utility regulator said Nov. 12.

Modeled after the state’s Successor Solar Incentive program, or SuSI, the New Jersey Storage Incentive Program would benefit privately owned, standalone energy storage installations and solar-plus-storage systems not eligible for storage incentives through SuSI, the New Jersey Board of Public Utilities said.

The BPU is hosting a virtual stakeholder information session on the proposed incentives Wednesday and will accept public comments through Dec. 18. It expects to launch the grid-connected incentive program early next year and the behind-the-meter incentive program in 2026, according to a public notice.

The BPU “proposes to interpret the [2030 storage mandate] as requiring New Jersey to procure 2,000 MW of storage systems capable of four hours of continuous discharge, or 8,000 MWh,” it said in the public notice.

For the purposes of counting toward the 2030 mandate, the BPU said it would derate the nameplate capacity of any storage system designed for a shorter discharge duration to reflect its maximum potential discharge rate over a four-hour period. For example, a 10-MW/20-MWh system designed for two-hour discharge would have an effective nameplate capacity of 5 MW.

The NJ SIP proposal envisions separate financial incentives for front-of-the-meter “grid supply” and distributed, behind-the-meter energy storage installations placed in service by Dec. 31, 2030, the BPU said.

Front-of-the-meter systems would be eligible for fixed incentive payments awarded annually through a competitive bidding process. In the future, front-of-the-meter systems could also be eligible for performance payments based on avoided greenhouse gas emissions if reliable day-ahead emissions data becomes available for generation assets in the PJM Interconnection, the BPU said.

Distributed systems would be eligible for annual fixed incentives through block grants and for performance incentives awarded by their electric distribution companies for successful reductions in on-site load or exports to the local power grid during periods of peak demand, the BPU said.

Distributed systems enrolled in the first incentive block could be eligible for an initial incentive of $150/kW to $300/kW in combined upfront and performance payments, depending on system size. Systems sited in “overburdened communities” characterized by relatively high rates of poverty, residents of color or residents with limited English proficiency would be eligible for an additional upfront incentive of $50/kW to $100/kW, depending on system size, BPU said.

The performance mechanism for calling distributed storage systems into service could take up to a year to develop following the debut of the grid supply incentive program, hence the expected 2026 launch date, the BPU said. The distributed-system incentive program would be modeled after the ConnectedSolutions program in Massachusetts and Connecticut, with the key difference that New Jersey electric distribution utilities will be permitted to set their own call hours and payments, the BPU said.

Eligibility for SIP incentives would not preclude energy storage system owners from earning revenue from the wholesale electricity market, participating in distributed energy resource aggregation services or using behind-the-meter assets “to actively manage their electricity usage at the distribution level and reduce electricity cost,” the BPU said.

Correction: A previous version of this story had an incorrect unit of measurement for New Jersey’s proposed energy storage incentive. It is $400/kWh

Article top image credit: onurdongel via Getty Images

Virtual power plants ‘well past pilot scale,’ but policy and tech challenges remain: WoodMac

Less than 20% of total DER capacity is VPP-enrolled, with residential thermostat and commercial and industrial demand response dominating, Wood Mackenzie found.

By: Brian Martucci• Published Aug. 22, 2024

Virtual power plants have moved “well past pilot scale in North America,” with 33 GW of capacity operating or in development across 1,459 deployments participating in 321 market, utility and retailer programs, Wood Mackenzie said in a July 29 report.

But enrolled VPP capacity accounts for only 19.5% of total distributed energy resource capacity, with legacy commercial and industrial demand response and residential thermostat programs accounting for a disproportionate share, WoodMac said.

Unlocking substantially more VPP potential requires a combination of effective program design, supportive state and federal policy, reduced barriers to wholesale market participation and wider adoption of advanced metering and home energy management technologies, said Ben Hertz-Shargel, global head of grid edge at Wood Mackenzie and lead author on its North America Virtual Power Plant Market 2024 report.

The report shows a surprisingly brisk pace of VPP adoption across North America, with more deployments and monetized programs than expected, Hertz-Shargel said.

“There is a lot more activity than people would believe,” he said.

But the headline numbers belie deep challenges around market access. A significant number of the 321 monetized programs identified in the report are bilateral VPP capacity procurements between VPP providers and load-serving entities, like utilities or retail electricity providers. Unlike programs offered to all eligible customers within a load-serving entity’s or system operator’s territory, these bilateral arrangements are closed to public participation, Hertz-Shargel said.

Market access is especially challenging for residential customers, the report found. Residential capacity accounted for less than 9% of total VPP capacity bid into wholesale markets, which Hertz-Shargel said underscored the segment’s unrealized potential.

“The rules of wholesale markets are not conducive to residential customers,” he said.

FERC Order 2222 was expected to improve wholesale market access for energy end-users, but the reality of the more than three years since its implementation has been more complex, Hertz-Shargel said. Echoing barriers identified by Guidehouse Insights in a January paper, the WoodMac report pointed to nodal aggregation restrictions that limit the potential size of individual VPP aggregations, poorly defined bidding and qualification rules, device-level data restrictions that drastically increase telemetry costs for small-resource aggregations, and state regulatory barriers to grid export compensation.

These barriers hinder customer adoption of economic demand response, or participation in day-ahead wholesale markets, according to the report. Only 17% of VPP capacity participates in day-ahead markets, which are essential for balancing the grid on a daily basis, Hertz-Shargel said.

The report identified recent state policy developments that could improve market access for customers and expand opportunities for VPP aggregators. Among the most promising were a Colorado law requiring Xcel Energy to deploy by February a performance-based VPP pilot program that accommodates aggregators and prioritizes avoided transmission and distribution costs; a Maryland law requiring utilities to establish programs compensating aggregators and DER owners for distribution system support services; the lifting of longstanding bans on third-party demand response aggregation in Michigan and Missouri; and New York’s Grid of the Future initiative to promote deployment of flexible resources.

Federal legislation introduced earlier this year by Illinois Democrats Sen. Dick Durbin and Rep. Sean Casten would eliminate the Federal Energy Regulatory Commission’s “opt-out” rule that enables more than a dozen state bans on third-party demand response aggregation.

“It’s notable that [policymakers] are starting to act at the aggregation level rather than the DER incentive level,” Hertz-Shargel said. “When states have taken action, it has resulted in programs that really work.”

The most effective VPP programs involve multiple resource types, rather than a single technology like thermostats, WoodMac found. Due to utility-imposed restrictions, programs run by utilities and load-serving entities themselves are much less likely to accommodate multiple technologies than bilateral capacity deals between load-serving entities and aggregators, the report said.

“We need more standard-offer programs where there is a clear price per kilowatt-hour and [VPP operators] can get creative to bring in customers,” Hertz-Shargel said.

Wider adoption of commercial building and home energy management systems will enable effective programming — and participation in day-ahead energy markets — according to WoodMac.

So will broader adoption of advanced metering technology, which could improve VPP capabilities and performance in former “laggard” markets now seeing investment in AMI 2.0 equipment, like ISO New England, Hertz-Shargel said. Until then, VPP program managers can make do with device-level data where utilities allow it, he added.

Article top image credit: Permission granted by sonnen, Inc.

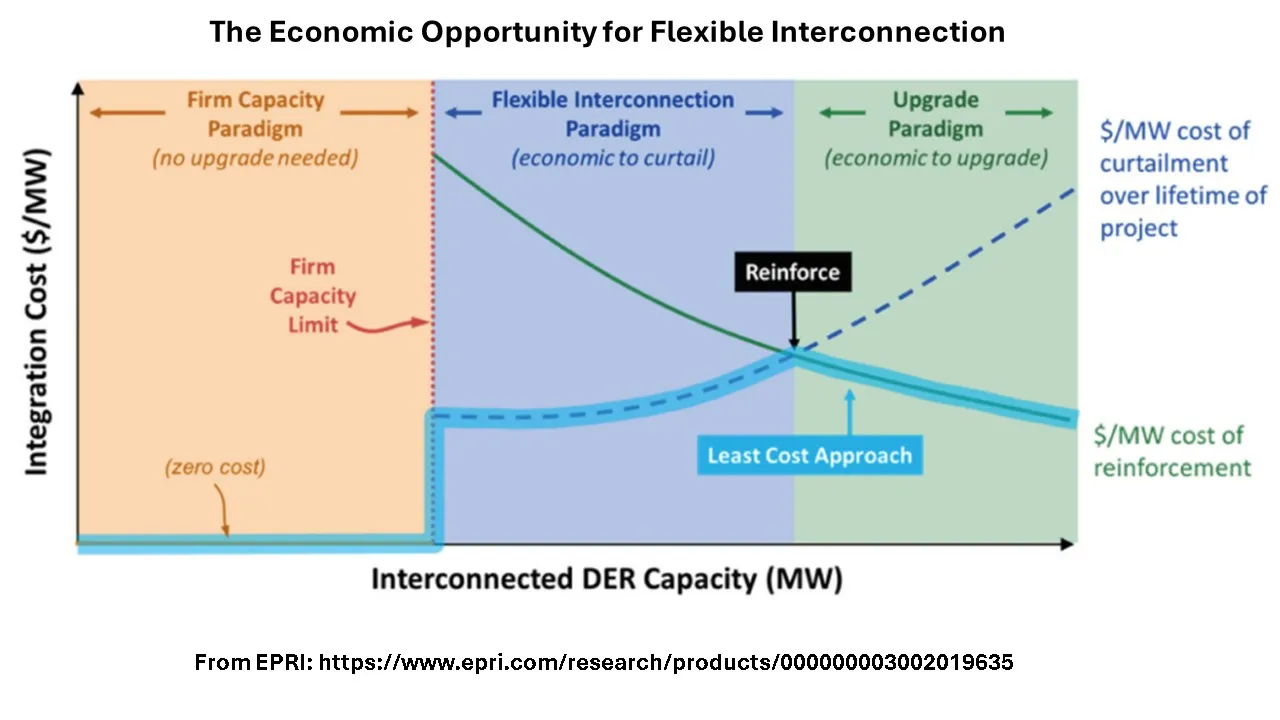

California pioneers new ways to ease interconnection of large DERs

Limited generation profiles in California will schedule limits to DERs during system constraints. New York, Illinois, Colorado and others are testing more flexible approaches.

By: Herman K. Trabish• Published Aug. 21, 2024

Efforts are accelerating to address the obstacles to interconnecting large distribution system resources like community solar and big box store rooftop solar arrays, advocates of recent reforms report.

Distribution system-connected resources, especially those in the 1 MW to 5 MW range, can offer flexibility to meet electricity demand spikes without requiring significant power system upgrades, the advocates said. But costs to increase system carrying capacity under current interconnection practices make many projects that require system upgrades uneconomic, they added.

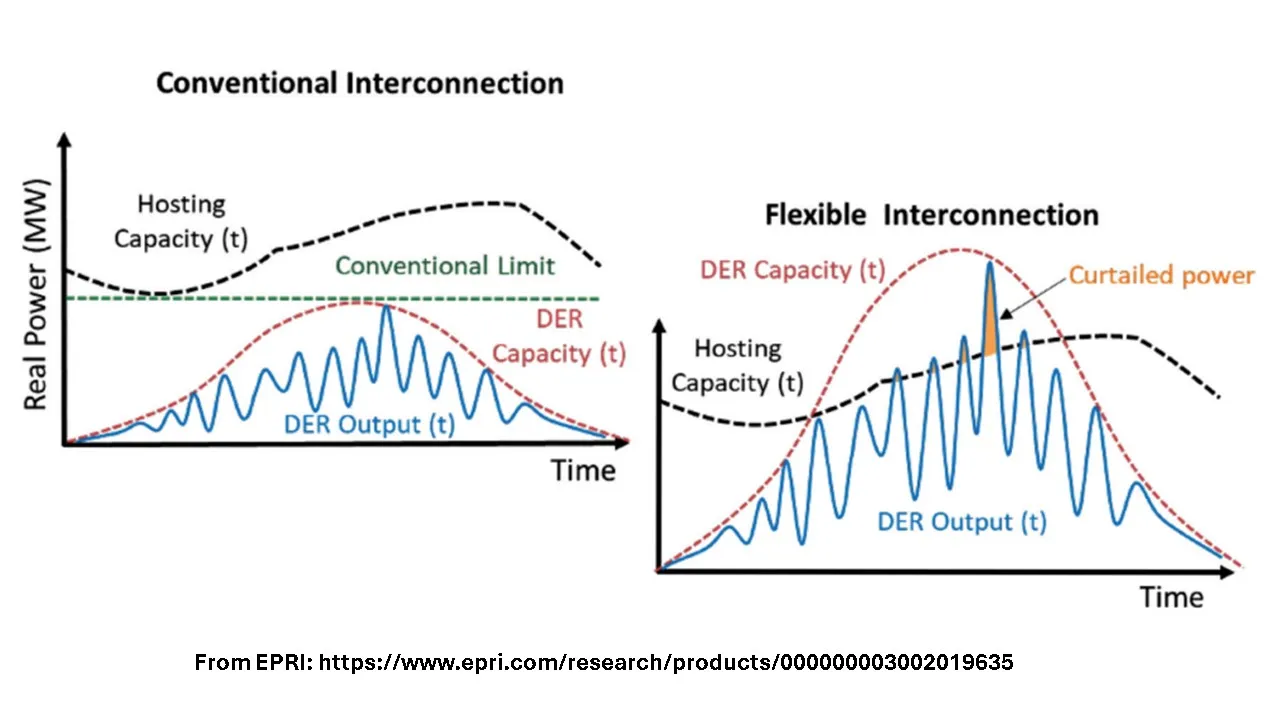

California’s limited generation profile, or LGP, option, approved March 24, will be the first state-wide implementation of the emerging “flexible interconnection” innovations for distribution system resources, which also include C&I customer-owned rooftop solar and solar plus battery systems, analysts and stakeholders agree.

The LGP option “allows developers to schedule export limits during periods of power system congestion to protect against overloads,” said Sky Stanfield, attorney for interconnection reform advocate Interstate Renewable Energy Council, or IREC, and a partner at Shute, Mihaly, and Weinberger. But losses from curtailed exports will be less than costs to upgrade power system carrying capacity, she added.

Policymakers in other states, including New York, Illinois and Colorado, are moving toward even more flexible interconnection practices for these large distribution system resources.

Flexible interconnections “pre-define” the annual percentage of curtailment, said Electric Power Research Institute Program Manager for DER Integration Nadav Enbar. The “central calculation” is whether the upgrade cost or the cost of unscheduled curtailments of generation from distribution system resources’ generation during periods of high power system carrying capacity congestion is more economic, he added.

Flexible interconnection options allow projects to interconnect faster by accepting limited curtailments, which supports achieving policy goals, advocates and analysts said. But the rapidly changing dynamics of U.S. distribution systems will make it challenging to protect reliability and keep developer costs predictable, they acknowledged.

The cost to interconnect

Anecdotal reports show new interconnection options for distribution system resources seem to be needed, though there is limited validating interconnection data to prove that need, stakeholders and analysts across the country agreed.

“As DER applications and penetrations rise, there tend to be more bottlenecks and longer timelines,” said IREC Director, Regulatory Program, Mari Hernandez. Public sources have reported distribution system interconnection backlogs in Maine, Massachusetts, Minnesota and other states, she added.

And a locationally-specific analysis showed a “more granular LGP” would add “significant” generation to the state’s power system, the California Public Advocates Office reported in April 2023.

The Department of Energy’s 2021 Solar Futures Study, which showed a potential for up to 200 GW of distributed U.S. solar by 2050, did not conclude anything about interconnection, acknowledged National Renewable Energy Laboratory Renewable Energy Policy and Market Analyst Manager Jeffrey Cook.

The best evidence that streamlined interconnection options are needed comes from project developers.

Distribution upgrade costs “are generally doubling developer costs in New York,” with some costs “increasing as much as six times,” reported Nexamp Director, Grid Integration Strategy and Policy, Benjamin Piiru. Without Illinois’s pilot flexible interconnection option, “we would have walked away from a project rather than pay for a $50 million upgrade,” he added.

California’s huge backlog of transmission system interconnection applications has impacted distribution system project interconnections, added Forefront Power Senior Manager, Market Development, Victoria Moroney. As a result, the vast majority of 1 MW to 5 MW projects are being delayed, and the LGP “can be a viable alternative,” she said.

The LGP option will be complicated and is only possible because of California investor-owned utilities’ years of work mapping their distribution systems, utilities and advocates said.

Permission granted by EPRI

Limited generation profiles

LGPs allow developers to voluntarily schedule reduced generation from their projects at times when congestion is expected at their locations on the power system rather than pay to expand system carrying capacity, IREC’s Stanfield said.

LGPs are possible because of monthly-updated, location-specific distribution system maps of hosting capacity analysis developed by California’s investor-owned utilities, Stanfield said.

Using them, California distributed energy resource providers “will for the first time in the U.S.” have the option to make the requirement to pay for increasing system carrying capacity unnecessary by “proposing an export schedule based on system conditions,” Stanfield said.

“Utilities will need assurances the necessary power control technologies are capable of maintaining developer commitments,” Stanfield acknowledged. The CPUC order postponed LGP implementation “until nine months after DER power control systems are certified” under Underwriters Laboratory, or UL, standard 3141, she added.

And with more LGP scheduling, changes in system load and supply could lead to new locations with congestion, Stanfield added. The CPUC addressed that by allowing utilities to curtail projects’ generation outside LGP schedules if there is a “sustained load reduction,” she said.

The CPUC order allows generation project owners to schedule two daily periods when their generation can be reduced below 100% of its capacity — based on patterns of distribution system capacity at the specific interconnection point, the CPUC decided. If changed monthly, that would create the maximum 24 changes in generation allowed for a project.

Southern California Edison believes LGPs can help meet clean energy goals and protect reliability, but they add “operational complexity,” Jeffrey Monford, the utility’s spokesperson, said. CPUC-ordered allowance of special load loss curtailments, required UL hardware certification, and limited scheduling changes will ensure reliability, he added.

But utilities “will still need to develop systems and operating practices to implement LGPs,” and that complex implementation will require “clear and timely” CPUC guidance, Monford said.

California’s LGP rule “is a great first step toward flexible interconnection” and “could be a gamechanger because it allows granular calculation of a project’s financial viability,” said Nexamp’s Piiru. But the developer’s decision “might be even easier under more flexible interconnection rules that set a specific maximum percent per year of curtailment,” he added.

More flexible interconnection rules are already being advanced, developers, utilities and analysts said.

Permission granted by EPRI

Even more flexibility

Timely and cost-effective interconnection can be done in ways that give developers greater benefits and utilities more control, most stakeholders agree.

Flexible interconnection is a spectrum of approaches that “may not always be the right choice but do expand project developer options,” said Coalition for Community Solar Access Senior Director, Interconnection and Grid Integration Policy, Samantha Weaver.

California’s LGPs are “one end of the spectrum,” and New York, Illinois and other states, are piloting more flexible approaches at “the other end of the spectrum,” Weaver said.

Flexible interconnection requires utilities to have advanced communications and DER management systems, or DERMS, “to handle unscheduled but capped curtailments,” Weaver continued. For those approaches, tariffs, curtailment rules and caps will be important, she added.

Commonwealth Edison’s flexible interconnection pilot “successfully enabled 6.75 MW of solar capacity,” with only 17 curtailment event days during seven months in 2022, reported David O’Dowd, the utility’s spokesperson. The pilot showed “curtailment events and duration are not broadly predictable,” and scheduling them “would result in unnecessary curtailment,” he added.

DERMS-managed flexible interconnection is also valuable because most states’ hosting capacity analyses , including those in New York and Illinois, are inadequate for interconnection, IREC’s Hernandez said. A national standard is needed to establish a requirement for how often data should be reported and how data reports can be validated for use in interconnection decisions, she added.

Cost sharing of upgrades could also be tested in pilots, Nexamp’s Piiru said. After multiple projects interconnect at a feeder and upgrades are needed, “all the developers, instead of just the last one to apply, could share the costs,” he added.

Xcel Energy’s flexible interconnection pilot anticipated Colorado Senate Bill 24-218, which calls for the state’s regulators and stakeholders “to modernize energy distribution systems,” said its lead sponsor, state Senator Chris Hansen, D. The bill was approved by Colorado Governor Jared Polis, D, on May 22.

The utility is reviewing existing policies and gathering stakeholder feedback, reported Xcel spokesperson Kevin Coss. It will finalize plans “for a small-scale demonstration pilot within the next six months” to evaluate “policy and technical considerations needed for a broader deployment,” he added.

“Flexible interconnection is a tool,” Senator Hansen said. “With growing curtailments in Colorado, it gives project developers an incentive to add storage options to increase the use of their generation during peak demand periods when generation is not curtailed, which increases the project’s value to the system and to DER builders and owners,” he added.

Ultimately, new technologies will be needed to resolve potential complexities in flexible interconnection approaches, Hansen, Xcel and others agreed.

DOE. (2024). “U.S. HCAs” [jpg]. Retrieved from DOE.

Still to be solved

Solutions that work for interconnection under some conditions may present impediments to interconnection under other conditions.

“The dynamics of power system operations make precise curtailment forecasting problematic,” EPRI’s Enbar said. “Even if a developer interconnects at an unconstrained location allowing full export, other interconnections there can eventually use all that feeder’s capacity, and require developers to pay for an upgrade,” he added.

But cost allocation between developers for upgrades “is not an easy question, because their revenues will be modified,” Enbar said. “Flexible interconnection can be an effective stop gap while the upgrade is built and cost allocation is worked out,” he said.

It will also be critical to define “the difference between curtailments from flexible interconnection and from a grid service program like demand response,” said Pacific Northwest National Laboratory Electricity Infrastructure and Buildings Division Principal Investigator and Project Manager Karyn Boenker.

“Developers with flexible interconnection agreements may face curtailments and financial losses, and demand response programs to protect system reliability are voluntary and compensated,” Boenker said. Policymakers must decide “how to separate compensation to each,” and regulators must decide “whether ratepayer or developers will pay” for the needed new technologies, she added.

But the current norm of relying on system upgrades “eliminates potential innovation,” said NREL’s Cook. “Interconnection processes can be tailored, and best practices will vary depending on the level of DER penetration, the utility, customer, and developer characteristics and preferences, the attributes of the electrical system, and other factors,” he added.

“There may be complicated puzzles to solve, but streamlined distribution system interconnection can save billions of dollars, reduce emissions and drastically improve reliability,” Colorado’s Sen. Hansen responded.

Article top image credit: FernandoAH via Getty Images

The rapid growth of distributed energy resources

Distributed energy resources, including rooftop solar, battery storage and electric vehicles, are experiencing significant growth in the U.S. as the power sector evolves to a cleaner, less centralized future. But what’s propelling the rise of distributed resources and what are the obstacles to more growth?

included in this trendline

FERC Order 2222 hurdles require new options for deploying aggregated DERs

California rooftop solar had a tough year following NEM 3.0. Can the industry bounce back?

Texas regulators look to expand successful 80 MW virtual power plant pilot

Our Trendlines go deep on the biggest trends. These special reports, produced by our team of award-winning journalists, help business leaders understand how their industries are changing.